My left eye -- revisited

How Obamacare saved my sight in a decade-long fight now happily concluded

I am reposting this reader-favorite from last September because I have happy news to share: my venous occlusion (hemorrhaging inside the left eye) seems to have been permanently addressed by the injections I started roughly a decade ago in a last-ditch attempt to restore my sight there.

When I began, I had to get injected every four weeks. I was not expected to recover because of a healthcare-related delay in my seeking treatment (too far gone — captured in the re-post below), but we tried anyway.

Last week I saw my retinologist here in Ohio. By agreement, it was 14 weeks since my last shot and there was no appreciable bleeding/distortion inside my eye. I had thus registered well over a year at 12-weeks-or-longer-between-shots without any reoccurrence.

In effect, I am considered cured — or perhaps better said stable. I will keep an eye on it (the other one) and I will likely check in with a retinologist at even longer intervals to stay on top of its possible return. But, yeah, this is a happy time for me on that score.

And I really need it with the work changes, our plan to sell our house here in Ohio and move back to the Midwest (no, Ohio is not Midwest), various life issues of being a parent to six (two still in HS and one just graduating college).

At age 62, I recently managed two falls: one off the back of the Penske truck we used to move household goods to Minnesota, and another when a boot lace got snagged while I was shoveling snow (always tie your laces!). Both were icy conditions and, in both instances, I was just this much too slow in my reactions, ending up with a severely dislocated index finger (left hand) as I failed to nail the landing off the truck (I should have attempted a multifinger landing) , and then later, when shoveling, a 3-stitch gash across my left forehead.

I know, I see the pattern too: left bad, getting older.

Anyway, those two events were brutally humbling, despite my success in moving half our household goods in a Penske during a vast snowstorm and super-cold temps around New Year’s — without a scratch to anything or anyone else!

It’s just that feeling of being that bit more vulnerable in your daily life.

So, sure, I went back to yoga for balance (and to restore half an inch to my height almost immediately), and I’ve been careful on my Trek cycle (only dry trail days, keep it under 20mph), but having these two trips to the ER happen in succession, amidst the move, prepping the house, shifting employers … and then the unleashing of Trump 2.0, I am feeling very much the proverbial cat on a hot tin roof.

And then I got this news about my left eye, and I immediately thought: corner turned!

It is possible that a blow to my head originally triggered the bleeding way back when, so where I managed to earn that nifty scare just above my left eye in January, I was pretty concerned I’d see a lot of bleeding in my eye this last go-around. So, imagine my relief to get the opposite news!

I am literally a cockeyed optimist in that my right eye is significantly higher than my left one, which means I can never see out of binoculars and need prism lens to correct. But I like to think of myself as figuratively one regardless of my sight, and there was some genuine faith in the future that was restored by this happy development.

And so I felt like sharing that today because good news right now is scarce as worries pile up and instabilities spread.

Anyway … something to make you feel better … my always sought-out happy ending.

NOTE: I need to publicly thank my brother Ted, the ophthalmologist/ glaucoma specialist, who, when I spoke with him about my eye issue back in the day, convinced me to see a retinologist in Wisconsin.

[The post from last September with the larger story

About a decade ago, I lost my employment-based healthcare during a time when I had my spouse in grad school, one kid in college, and four others in a Catholic grade school. Of course, the bigger and more immediate problem was replacing the lost income, so I threw myself into that with complete abandon — as in, literally working around the clock.

But the healthcare thing was scary. Because I had had some issues in the previous five years (kidney stones), my applications for individual family coverage kept getting rejected. Finally, I was advised to go with Obamacare, which I did, but it took a while to set up, meaning there were months where we had nothing once the COBRA extension ran out. For a family that once battled a childhood cancer for a couple of years, that was deeply scary.

Once we got Obamacare set up as our last resort, I finally went in and saw a retinologist in the U. Wisconsin healthcare system about an issue that had been flagged about a year earlier during a routine eye exam. I had been told that I had suffered some sort of damage to veins in my left eye and that the resulting swelling (internal bleeding) was distorting my focal point in the back of my eye.

The optometrist basically said that the damage was done and I was just going to have to live with it, making it sound not so bad because my right eye was overperforming and keeping my overall corrected vision good. But, eventually, I was told, my left eye would become rather useless.

The optometrist gave me the wrong impression of where I was in this situation, and the casualness of the information delivery incorrectly led me to believe that there wasn’t much I could do other than monitor. As that advice hit right around the time we lost insurance, I filed it away mentally and then focused on getting other, more immediate problems solved before things settled down enough for me to finally see a retinologist, who are typically hard to schedule, like any specialist.

When I finally saw someone, I was told that the damage was beyond repair — in all likelihood, and man, it was too bad I didn’t come in earlier because it might have been addressed with some success if we had just caught it in time!

Under normal circumstances (no loss of work-related insurance), I would have seen this guy a year earlier than I did. Instead, I did the dad-thing, as I felt I should, and made sure my spouse and kids’ lives were as little disrupted and threatened as possible.

Yea for me, bad for my left eye.

And yeah, I was feeling totally f—ked over by events.

At the time, I remember thinking to myself that this sort of thing must happen all the time to people who lose insurance like we did — just bad timing and poof! There goes your vision in your left eye as penalty.

Who knows what we’ll take from you next time!

But what I remember more was the fear — that sense of profound vulnerability.

Looking back, all I can say is thank God for Obamacare. It was the only option out there that said yes during our time of need, and, with the subsidy, I could just afford it at the time. We were on it for about 15 months until my spouse graduated and got us on her job’s coverage.

And during those 15 months?

During those 15 months I started getting injections into my left eye. I was told it was super expensive (like $4k a shot) but covered under my insurance. I was also told it would likely not work at all — just too much damage and too much delay in dealing with it. But, what the hell, why not give it a try?

Well, the drug worked, shrinking down the swelling and somehow tamping down on the hemorrhaging going on inside my eyeball. The shots were deeply unpleasant, but, when that’s the choice, you submit.

At first I had to have the injection every four weeks. Now, almost a decade later, I get one every 12 weeks or so, and my current retinologist says we may experiment with dropping the injections altogether later this year and see if things hold steady.

The injections, by the way, have gotten dramatically easier thanks to new procedures and anesthetics. I fly right through them nowadays. Yes, a few hours later after the drugs wear off, it still seems like somebody just punched me in the eye, but that’s nothing.

Now, if I close my right eye and look only through my left, I have a pretty clear field of vision. Can’t read normal sized text to save my life, but, all in all, an unusually solid recovery for which I remain deeply grateful.

A GOP win this November is estimated to kick a lot of Americans off Obamacare. This scenario naturally rings a lot of bells for me.

From the cited WAPO op-ed

The uninsured rate remained steady last year, at roughly the lowest level ever recorded. That’s a small miracle — but one that could vanish if lawmakers don’t act soon.

The share of Americans without health insurance coverage was just 8 percent in 2023, statistically indistinguishable from the record low reached the prior year (7.9 percent), the Census Bureau reportedTuesday. For context, in the bad, old pre-Obamacare days, the share of Americans lacking health insurance was roughly double that amount.

It’s not perfection, but it’s progress. And it’s largely due to a stealth Obamacare expansion that Democrats recently engineered through the tax code.

From an NYT story, this is what Obamacare has provided:

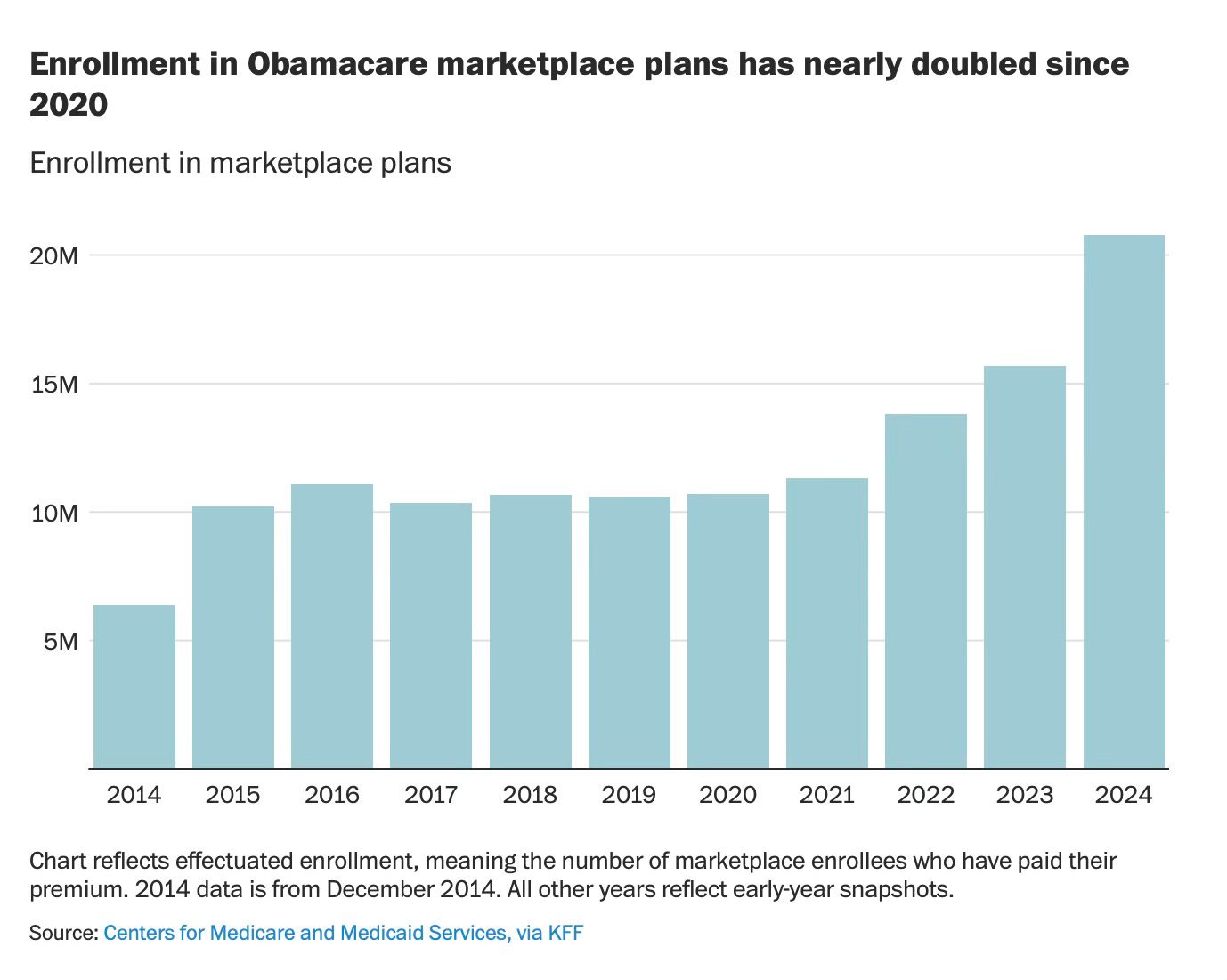

Nearly 50 million Americans have been covered by health insurance plans through the Affordable Care Act’s marketplaces since they opened a decade ago, according to tax data analyzed by the Treasury Department and published on Tuesday.

Federal officials said that the findings represent roughly one in seven U.S. residents, a broad swath of the population that underscores the vast, and seemingly irreversible, reach of the 2010 law.

Naturally, given Trump’s many attempts to kill Obamacare during his term, the Dems fear more assaults are guaranteed if he gets back into office — a subject about which Trump has remained purposefully vague. A renewed Trump administration wouldn’t necessarily need to repeal the law. Instead, it could simply let those Dem-engineered tax breaks expire, thus indirectly starve Obamacare out of existence.

God forbid Trump’s tax cut for billionaires should similarly expire!

Recall: in October of 2017, the Trump Administration killed the original Obamacare subsidies that benefited my family so much in our time of need, claiming the cost-sharing reduction (CSR) payments were unlawful. That led to all sorts of lawsuits and state and local efforts (largely among the Dems) to work around that shortfall. CSR payments were never reinstated, and the insurance market adapted through premium adjustments and other strategies to cope with the absence of federal funding.

Per the WAPO op-ed:

In laws enacted in 2021 and 2022, President Joe Biden and Democratic lawmakers increased tax credits that Americans could claim for premiums on individual marketplace plans. These measures didn’t receive a ton of media attention at the time, especially relative to sexier programs bundled into the same bills, such as stimulus checks and climate subsidies. But the tax changes nonetheless made a huge difference in access to health care for tens of millions of Americans, and they became an unsung hero of the affordability crisis.

Enrollment in Obamacare has doubled under Biden, with most of them being from the lowest income brackets.

So, what’s expected in a second Trump administration? Or maybe just a Senate captured by the GOP?

Still in WAPO:

Unfortunately, all this progress is at risk.

That’s because the expanded premium subsidies are scheduled to expire in December 2025, unless lawmakers intervene to extend them. Lawmakers are expected to haggle over the program at the end of next year, when many other parts of the tax code expire, too. But Congress really ought to act before then because insurers will start pricing and advertising their next set of premiums earlier in the year. And if lawmakers allow the tax credits to sunset as scheduled, health-care premiums will likely spike.

Oddly, this ticking time bomb has gotten little attention in the election thus far, especially compared with other tax-related issues that affect a much narrower slice of voters.

So, here’s the fear:

Nearly 20 million Americans will see their premiums go up if those tax credits lapse as scheduled. Even worse, 4 million people would lose coverage entirely, the Urban Institute estimates. Moreover, those numbers are just snapshots of marketplace participants at a given moment; they don’t capture the entire universe of Americans who have ever needed (or might yet need) marketplace coverage, which often serves as a stopgap between jobs or other health plans.

That last line was essentially my family about a decade ago.

If you want to know what another Trump presidency would foretell, look to his Republican allies in Congress. They say openly they want these subsidies to expire — and therefore, to let premiums spike. In fact, the Republican-run House Budget Committee’s budget last year proposed rolling back the subsidies earlier than scheduled. Since then, proposals to extend the program have been roundly criticized by Sen. Mike Crapo (Idaho) and Rep. Jason T. Smith (Mo.), the lawmakers expected to run tax negotiations next year if Republicans control both chambers of Congress.

Brutal stuff, if you’re ever so unlucky to find yourself on the receiving end.

Me? Every morning when I wake up and realize I can still see out of my left eye, I thank Barack Obama for the effort, along with everyone who’s kept Obamacare going ever since (H/T John McCain).

My brother was an Eligibility Specialist for RI's Obamacare exchange, "HealthSource RI," when it rolled out. He said his training classmates and he sensed it was a historical moment they were participating in, and stories like yours were legion just among the customers he helped.

Congratulations 👏. Fantastic news.