This is a reader-supported publication. I give it all away for free but could really use your support if you want me to keep doing this.

My spouse and I cannot sell our house in a village where — until Trump was inaugurated — the average house stood for sale a whopping 5 days before being snatched up (Yellow Springs OH has historically been that popular.) We’ve come down 17% on the price since putting the house up for sale in late February and we’ve yet to receive one offer. Plenty of showings, but no offers.

Why?

Realtors all say the same thing: People are super reluctant to purchase a home right now due to all the economic uncertainty associated with Trump 2.0, and those willing to take that plunge are beyond picky, as in, it needs to be both a steal on price and walk-in-ready (two attributes that almost never are paired). In reply, homeowners are de-listing at record rates (pulling houses off market). We are likely to make the same move shortly enough.

I will admit to some ambivalence on being so thwarted: plenty of good reasons to stay another year in Ohio but plenty also to moving to Minnesota this year.

That’s our problem, or just call.

But to have the Zillow calculated value of your home drop that 17% over just the opening months of the Trump administration (hence our corresponding price adjustments)… that stings.

Yes, yes, there is complex causality at-work here but there’s also that inescapable truth: economic uncertainty has skyrocketed under Trump and an immediate victim is the already troubled housing market (see, skyrocketing insurance rates). I mean, the whole system said our house was worth yea much on 20 January and now the whole system says … take 17% off the top if you hope to sell.

I learned long ago not to view home ownership as a wealth generator, unless you’re willing to sit in the same house for decades (alas, not in my nature or my spouse’s), but it remains stunning to me that one man’s decision-making can alter so many lives so negatively at such speed by creating such individual-level economic uncertainty and fear while, BTW, jacking up the price of money (borrowing) — all in this magical quest to return America to some 1950s fantasyland where we dominate global manufacturing.

Jim Nuttle illustration from “America’s New Map”

Which gets me to this gnawing sense of doom that is the primary driver of my desire to stop owning a home this year ASAP: I have a hard time seeing a better functioning US economy in coming years, so long as we remain on this chaotic track.

I know, I know, I’ll be told to wait for it … wait for it!

But, let’s be honest, Trump is never NOT in chaos mode — that’s his superpower (very dictator-y, I will note). So, this idea that, if we can just stand a bit of uncertainty in our economy for a stretch, then it’ll all turn out right … that seems truly nuts.

The guy is famous for running businesses into the ground and defaulting on his debts.

This same guy seems to running the US economy into the ground and setting up the USG to default on its debts.

Trump is entirely comfortable with all this because, in his mind, so long as it seems like he’s winning (spinning not included), then he’s successful. He really doesn’t care whatsoever about the actual outcomes, which is what makes him a true supervillain — right down to his penchant for bizarre monologuing.

The White House cites strong job growth, rising wages, and robust private sector performance.

However, the economic data and independent forecasts says something else.

Our economy contracted at an annualized rate of 0.5% in the first quarter of the year — the first time that’s happened in three years. But even that masked a weird surge of imports ahead of anticipated tariffs and people consuming less — out of fear (putting off big purchases being the sine qua non of the angst).

Despite all the tumult in DC with the federal government, the unemployment rate remains steady, even as most of us understand that that rate includes a lot of people working in an under-employed/under-compensated manner relative to their expectations or recent past. Job growth is down relative to 2024, and when pollsters ask people if they’re employed as they would care to be, then we find that a frightening majority of workers (80%) feel themselves presently abused or thwarted by their employers.

So far, the big win for Trump is the continued slowing of inflation — and yet, here come the new/resumed tariffs threats, which Wall Street continues to blow off (lucky them), while everyone not directly employed by Trump are saying we’re looking at seriously higher prices for the second half of this year, to include a lowering of GDP growth. The dreamt-of gains in manufacturing aren’t appearing on anyone’s reasonable time horizon. Meanwhile, construction and agriculture are suffering (lost migrant labor) and the US housing market seems poised for a crash on the insurance issue alone (not an issue to the Trump people because climate change isn’t real).

All the Trump declarations of “record” business investment are mostly about claiming what was already in the pipeline under Biden. In truth, business are playing it extremely safe right now — just like potential home buyers.

After Biden gave us 2.4% GDP growth last year, almost nobody sees us above 2% for 2025. And, for beyond that … let’s hope the world keeps buying our sovereign debt while Trump trashes the global trade order upon which the rest of the world so dearly depends.

Simply put, America is bleeding international goodwill right now — profusely.

For the moment, businesses, households and financial markets are locked in an elaborate game of wait-and-see. Companies stocked up heavily early in the year in anticipation of tariffs. Indeed, they did so by enough to drag measured gdp growth into the red in the first quarter, as a surge of imports distorted the numbers.

These stockpiles will be run down. In many cases, they have already been depleted, meaning that businesses are turning once again to imports. Last month customs duties were more than three times as high as the average in recent years. Companies that bring in goods from abroad now face an unpalatable choice: either they can eat the tariffs and accept lower profits, or they can pass on the additional costs to their customers.

So far, they have mostly chosen the first option. Bosses are attempting to wait out the president.

We’ve all just been enjoying this lengthy fuse, hoping for no negative “boom” at its climax. But, as we all know, Trump is the master of delaying and goal post-moving, so who knows how long this wait-and-see stuff goes on because we all know he likes it that way.

Then there’s just the general feeling that extends beyond the executives and bosses down to us regular folk: the waiting out of Trump.

We did that for four years and it exhausted us. Most of us are already exhausted with Trump 2.0 and we have three-and-a-half-years still to go.

But, beyond that, doesn’t it just seem wrong in this world and era of ours that our primary instinct is to wait out our own political leadership?

I mean, that seems like something more Chinese or Russian in nature — as least in historical terms. But, now we’re in the same boat.

So, this is all in God’s hands, which is what one turns to when patriotism itself offers insufficient refuge from reality.

Back to The Economist:

Oddly, though, tariffs may be pushing down prices via another mechanism—by taking a toll on the economy. The Liberation Day drama crushed consumer confidence, possibly softening demand. Until recently, this has been evident only in “soft” data (surveys and the like). Now signs of it are starting to appear in “hard” data, too. A recent release showed that household spending fell month-on-month in May. Employment figures for June were strong, but bolstered by government hiring, especially of teachers. Those for the private sector were lower than expected.

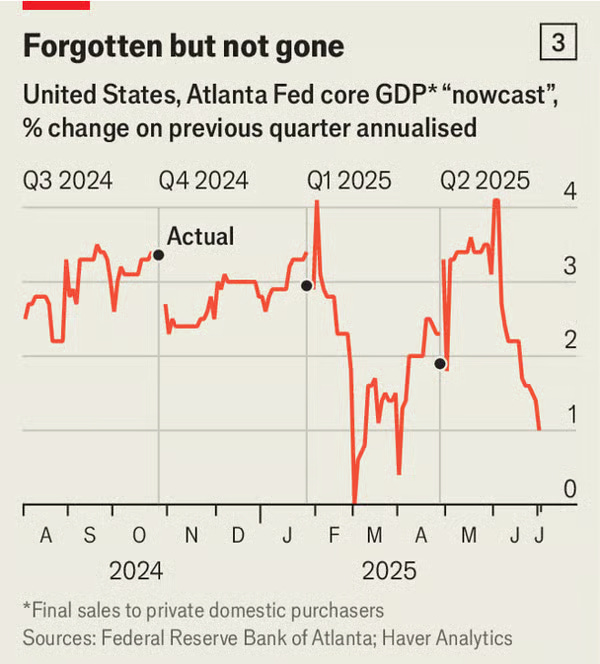

A running estimate of gdp, produced by the Fed’s Atlanta branch, suggests that its core components (private investment and consumption) have fallen from an annualised growth rate of 2-3% at the start of the second quarter to 1% now (see chart 3). Goldman Sachs, a bank, has compared the latest data to previous “event driven” shocks that led to recessions, and found that today’s slowdown is roughly in line with the historical norm.

To me, that sounds like we’re waiting for a recession or a period of significant and lengthy stagnation that looks like ….

Wait for it … an American version of BREXIT but one attempted at a global scale (withdrawal from the international liberal trade order — that we created, BTW):

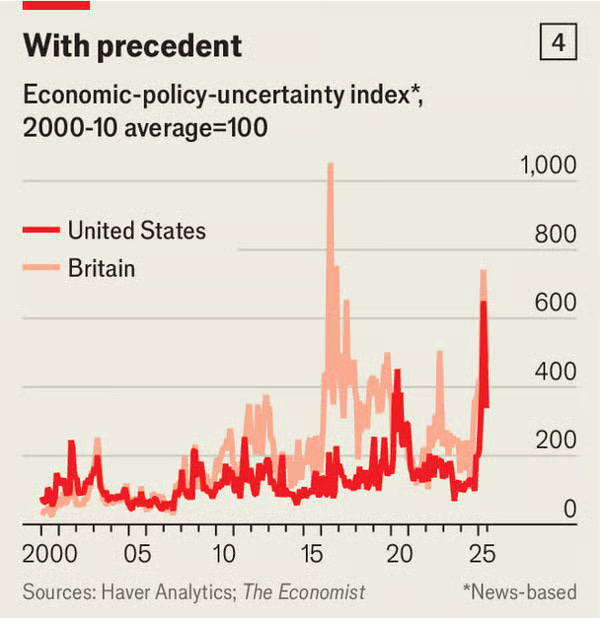

Whether this is the start of something more serious depends, in large part, on quite how punchy the president feels on August 1st. Without another deadline extension or similar, a further slowdown seems likely. Moreover, as Britain discovered after leaving the European Union—the most recent case of a rich country imposing large trade barriers on itself—elevated uncertainty can by itself be sufficient to suppress business investment for quite some time. And America is now an extremely uncertain country (see chart 4)

The Economist’s glimmer of optimism rests on the underlying strength of the economy that Trump inherited from Biden (irony of ironies):

Tariffs are colliding with an American economy that is, by any historical or international standard, extraordinarily dynamic. It has been growing at a consistent 2-3% a year since 2022. As a consequence, America is one of the few rich countries that might be able to shoulder even a sizeable hit to its growth without falling into recession. The additional stimulus in Mr Trump’s “Big, Beautiful Bill” is also front-loaded, meaning that it will provide a boost this year and next, which could help obscure the impact of tariffs (even if it also creates an inflationary mess for the Fed to handle). All this suggests a future in which economists endlessly debate the actual impact of the tariffs, while the American public barely notices them, despite having been left poorer. Not a triumph for Mr Trump—but not a disaster either.

To me, this is classic business Trump: Pretend like the rules don’t apply to him. Load up on debt and push that reckoning day past some exit deadline (here, Constitutional, thank God), and then publicize and spin the hell out of the whole package, pretending it’s a great success when, in truth, he’s just kicked the can down the road past January 2029 while torching a boatload of allied relationships across the planet.

In other words, we’re being treated to a true bread-and-circuses show that’s more likely to trigger a steep superpower decline in its wake than any magical return to Trump’s idealized 1950s childhood.

Everyone went into the 2024 election knowing Trump is the ultimate flimflam man, and he’s is living up to his carved-in-stone reputation.

Meanwhile, ask yourself: Do you really think we’ll be better off economically on this track come January 2029? Do you think we’ll “catch” China or fall further behind in key industries that the world sees as representing the future but MAGA sees as “evil”?

This is why I want to end my latest risk-exposure known as home ownership: I spot the same sort of superpower suicide trajectory in both Trump’s foreign and domestic policies.

The BREXIT analogy seems apt: one massive own-goal from which we may well never recover — certainly at least as a superpower.

And won’t that be the Boomer coup de grace? Their appearance coincided with, and benefitted greatly from, America’s emergence as a global superpower in the aftermath of WWII.

And now, thanks to four more years of Boomer presidency, those same Boomers will exit stage right just as America’s superpower status is completely trashed.

In the end, I guess, America being a superpower was just the Boomers’ historical birthright/toy. They’re leaving the playground in a huff right now and they’ve decided to take their ball with them.

There is your Trumpist legacy.

Losing some money on a house sale? That’s trivial

Losing our superpower status — by choice, that’s a God-damn tragedy.

Respectfully, dear Mr Barnett, WHAT EXACTLY do you have against simple-minded, bone-headed, own foot-shooting, hyper-bellicose claptrap? ... Oh, and didn't super-severe, monster badass warrior/senator Tom Cotton himself PROVE America's "global brexit" is in fact a GOOD THING? ... Lastly, a request, sir: please use your considerable INFLUENCER status to END that insidious & sophomoric slur that SecDef Hegseth is a "BIMBO WARRIOR"? (What's that even supposed to mean???) ... Not nice, nor helpful & one more time, very, very juvenile. . Regardless, for the record (and as HughHewitt reportedly repeatedly attests): Pete Hegseth is not only NOT a "bimbo warrior," he is Sooooooo NOT A BIMBO WARRIOR!

In personnel terms, it's garbage in, garbage out.

Respectfully, dear Mr Barnett, WHAT EXACTLY do you have against simple-minded, bone-headed, own foot-shooting, hyper-bellicose claptrap? ... Oh, and didn't super-severe, monster badass warrior/senator Tom Cotton himself PROVE America's "global brexit" is in fact a GOOD THING? ... Lastly, a request, sir: please use your considerable INFLUENCER status to END that insidious & sophomoric slur that SecDef Hegseth is a "BIMBO WARRIOR"? (What's that even supposed to mean???) ... Not nice, nor helpful & one more time, very, very juvenile. . Regardless, for the record (and as HughHewitt reportedly repeatedly attests): Pete Hegseth is not only NOT a "bimbo warrior," he is Sooooooo NOT A BIMBO WARRIOR!